Most people dream of being rich. Few think about being wealthy.

The difference? Richness is loud — expensive cars, designer clothes, exotic holidays. Wealth is quiet — investments, assets, and the freedom to never worry about the next payday.

To understand why this difference matters for your financial wellbeing, let’s meet four very different people, each living a very different version of “success.”

How Much They Earn?

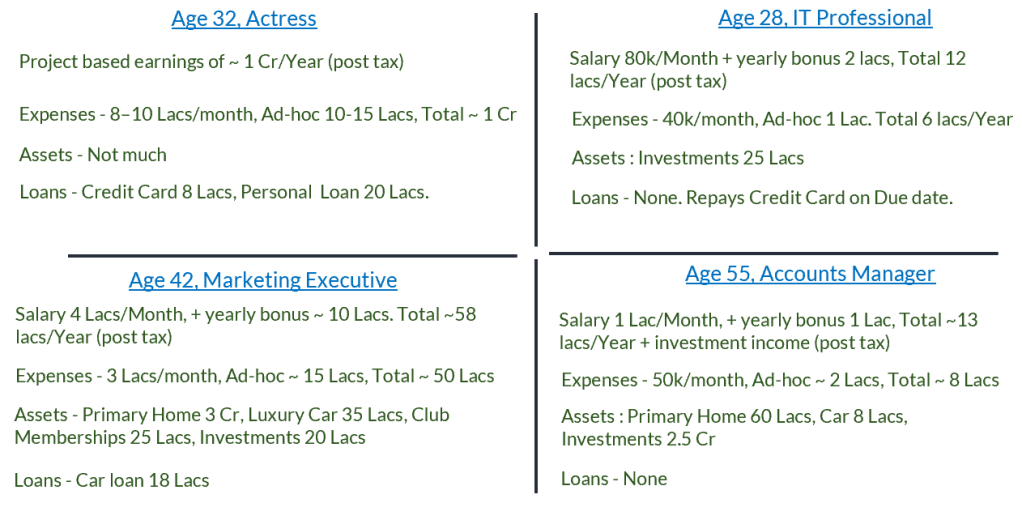

The actress earns around ₹1 crore a year. However, her income is irregular, tied to projects and performances. The other three earn fixed monthly salaries and annual bonuses. For simplicity, let’s assume these are post tax numbers.

Spending Patterns

- Actress: Her high lifestyle demands—paying 3 lacs in rent, spending on fitness, designer clothes, stylists and staff fees, beauty treatments, social appearances. Her monthly expenses pile up to ₹8–10 lacs. Add ₹10–15 lacs for vacations and total yearly spend becomes nearly ₹1 crore.

- IT professional: He lives with parents, contributes to household expenses, yet manages to keep his monthly spend below ₹40K. Occasional splurges on travel or gadgets average around ₹1 lac in a year. Total spend: ~₹6 lacs.

- Marketing Executive: He has to maintain a high lifestyle, monthly maintenance for his home is more than what many people spend on a rent, sizable portion of his salary goes towards premium schooling of his children, then there are weekly parties and networking, all of that adds up to ₹ 3 lacs of spending per month. Add ₹10–15 lac for vacations, luxury watches and latest gazettes. Total spend in a year is ~₹50 lacs.

- The Accounts Manager maintains a modest lifestyle. Monthly spend is ₹ 50,000 plus one off expenses of ₹2 lacs making his yearly spending ~ ₹8 lacs.

Financial Position

- The Actress spends nearly all she earns. No savings. No assets. Irregular income forces her to rely on credit cards and personal loans.

- The IT Professional saves 50% of his income, ₹6 lacs every year. He started investing early and has built up investment portfolio of ₹25 lacs.

- Marketing Executive manages to save ~ ₹8 lacs per year. And he has used those savings to buy a beautiful home for ₹3 crore, a luxury car and a few club memberships. His investment Portfolio which mostly comprises of provident fund is close to ₹20 lacs. And he has an outstanding car loan of ₹18 lacs.

- The Accounts Manager saves ₹5 lacs annually, owns a modest home and car, and has built a ₹2.5 crore investment portfolio

So, who’s doing better financially?

True Measure of Wealth

At first glance, the Actress looks “rich.” The Marketing Executive seems successful too — after all, he earns the most among the salaried ones.

But there is a difference between being Rich and Being Wealthy

Rich refers to having a high income to fund your expenses. The signs of being rich are visible. People can see your house, your car, your shoes and clothes.

However, someone who appears rich because of their latest car, branded suites or fancy vacation pictures might actually be living salary to salary.

Wealth on the other hand is the money that you haven’t spent. It’s the money you’ve saved and invested, that may not be visible to outsiders but still provides you the financial independence and peace of mind.

So the right yardstick to measure your financial wellbeing is your financial networth. Financial networth is your financial assets less your liabilities.

In our example, the actress has no assets but loans worth ₹ 20 lacs, resulting in negative networth. She is highly dependent on timely and continued income to manage her daily life.

On the other hand the IT professional has a networth of ₹ 25 lacs, which will be sufficient for him to fund next 4 years of his living expenses or fund any other life goals.

The marketing executive manages to save highest amongst the four. But he has used those savings mostly for buying ‘consumption assets’. A primary residence is essential, but it doesn’t generate income — and in normal situations, you would not think of selling it to fund your lifestyle. Other assets are depreciating assets and may not get the same value if he wants to sell those. That’s why these are considered consumption not financial assets. His financial assets are ₹ 20 lacs against the loan of ₹ 18 lacs, making his networth just ₹ 2 lacs, less than his monthly salary.

Whereas the wise accountant has a networth of ₹ 2.5 cr, in spite of having less than one fourth salary compared to the marketing executive.

Key Components of Building Wealth

There are four important components of building wealth.

- How much you earn

- How much you spend and save

- What kind of assets you invest in

- what kind of liabilities you have

Often people focus on just a single aspect, either chasing higher income but without any attention to savings or some people try to save as much as possible without realizing that, the same energy if focused on increasing earnings would give better results.

My Advice

In the early years of your career focus on growing your income by learning skills and advancing in your field.

As your income grows:

- Control lifestyle inflation, so your expenses don’t rise as fast as your salary.

- Invest in income-generating and appreciating assets, not just consumption items.

- Avoid debt that doesn’t create value.

At the end of the day, wealth isn’t about how much you earn — it’s about how long you can sustain your life without working.

Being rich can buy you nice things today. Being wealthy can buy you time, choices, and peace of mind for life.

So measure your success not by the size of your paycheque, but by the strength of your net worth. Your future self will thank you.

Leave a reply to Money Musings: What Financial Independence Really Means – VeridianFin Services Cancel reply